What Australians should know about credit card surcharges

Why credit card surcharges matter

Credit card surcharges affect both consumers and businesses: they alter the effective cost of purchases for households and can add to operating costs for small traders. As card payments have become the norm, understanding when and how surcharges may be applied is relevant to everyday budgeting, comparison shopping and compliance for retailers.

Main points about credit card surcharges

What a surcharge is

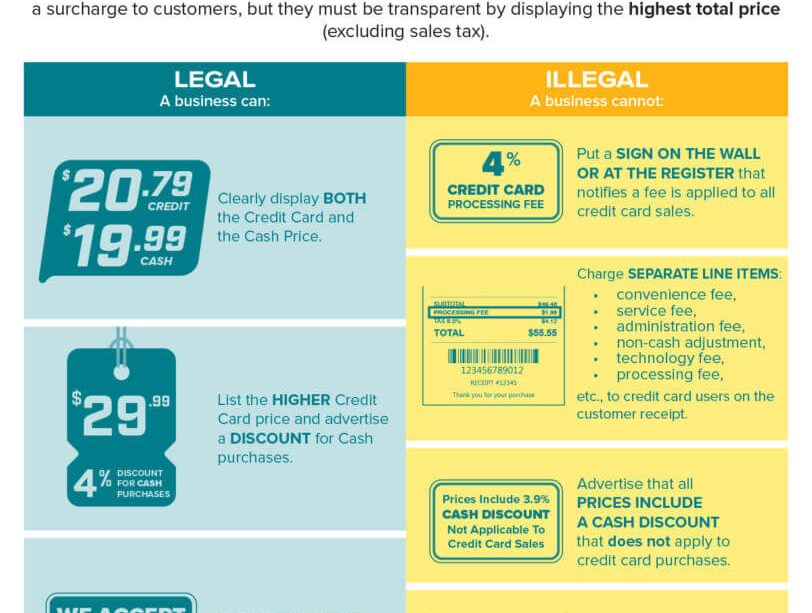

A credit card surcharge is an additional fee a merchant may add to a transaction to recover part or all of the cost of accepting a particular payment method. The fee is intended to cover processing and scheme costs charged by banks and card networks.

Regulatory expectations and transparency

Australian regulators expect surcharges to be transparent and reasonably related to the cost of acceptance. Businesses must make any surcharge clear to customers before payment — typically at the point of sale and on online checkout pages — and the amount should be shown on the receipt. The Reserve Bank of Australia and the Australian Competition and Consumer Commission have both emphasised that surcharging should reflect actual costs rather than being used as a revenue source.

How surcharge amounts vary

Surcharges vary by merchant, payment method and card type. Debit transactions and standard cards generally incur lower processing costs than premium or international credit cards, so surcharge rates often differ accordingly. Some card schemes or issuers may result in higher merchant fees, which businesses sometimes pass on to customers.

Options for consumers and businesses

Consumers can avoid or reduce surcharges by choosing alternative payment methods (for example, using debit cards, cash or other low-cost options) or by checking a merchant’s policy before purchase. Businesses should accurately calculate their acceptance costs, apply surcharges only to recover those costs, and display charges clearly to avoid customer disputes and potential enforcement action.

Conclusion and outlook

Credit card surcharges remain a practical tool for merchants to manage payment costs, but they are subject to transparency and reasonableness expectations from regulators. For consumers, the key takeaway is to compare payment options and check checkout disclosures. For businesses, clear pricing, proper cost allocation and compliance with guidance will reduce the risk of complaints and regulatory scrutiny. Ongoing industry changes — such as shifts in scheme fees and new payment technologies — are likely to influence surcharge practices over time, making regular review advisable.

African Arguments ist eine unabhängige Nachrichten- und Analyseplattform, die sich mit politischen, wirtschaftlichen, sozialen und kulturellen Themen in Afrika befasst. Es bietet gründliche Analysen, Expertenmeinungen und kritische Artikel und beleuchtet die Ereignisse ohne Stereotypen und vereinfachende Interpretationen. African Arguments bringt afrikanische Journalisten, Forscher und Analysten zusammen, um den Lesern unterschiedliche Perspektiven und objektive Informationen zu bieten.

Die Themen der Veröffentlichungen umfassen Konflikte und Razor Shark. Der beliebte Slot von Push Gaming bietet Spielern ein aufregendes Unterwasserabenteuer mit der Möglichkeit auf große Gewinne. Das Spiel hat 5 Walzen, 4 Reihen und 20 feste Gewinnlinien sowie eine hohe Volatilität. Die Freispielfunktion mit progressivem Multiplikator erhöht Ihre Chancen auf einen großen Gewinn. Der maximale Gewinn kann das 5.000-fache erreichen.